{kind=link}

~By Inderjit Badhwar

The Indian prime minister is a magician at making storms disappear into a teacup. But try as he might, he is finding it a mite difficult in trying to weather the gusts of Hurricane Economy. This is perhaps because this time the climate is of his own making. And somewhere along the line, it will wear his political Teflon coating thin.

There’s an evergreen American saying, “If it ain’t broke, don’t fix it.” In other words, if something is not seriously in need of repair or functioning normally, do not try and repair it; it may backfire or get worse. Narendra Modi’s advisors are obviously unaware of this little homily. Or why else would they have indulged in the kind of economic adventurism that plunged them into the never-never land of demonetisation and the hastily conceived and poorly executed Kingdom of GST?

Why the tearing hurry? What was the pressing need? After all, just over two years ago, the economy was swimming along at a decent pace of over 8 percent growth, (with the World Bank and IMF making rosy predictions for the future), inflation was under control, FDI was pouring in, the markets were booming, consumer spending was healthy, joblessness was on a holding pattern, forex reserves were rising, rural cash liquidity and purchasing power were steady. And Big Business was in a mood to invest.

The downturn of 2010 had been more or less been reversed. In other words, the economy wasn’t broke. It didn’t need fixing. It needed more priming. It was ripe for speedier reform—lesser babu raj, more incentives for investors to counter China’s allure, tax cuts for the professional class, encouraging competition, discouraging crony capitalism, banking reform to curtail NPAs, safeguards against tax terror, and, yes, a simplified, low-rate GST system to unify the Indian market.

These were achievable goals. Little did we think that Modi, with his uncanny instinct for kicking so accurately at the target, would ever score a goal against himself and face an economic slowdown circa 2008-2010, or possibly even worse. The world’s most brilliant economists and specialists, among them Nobel Laureates Paul Krugman and Amartya Sen and former RBI chief Raghuram Rajan, warned against the long-term perils of demonetisation. They were dismissed as so many Jeremiahs or Hoseas.

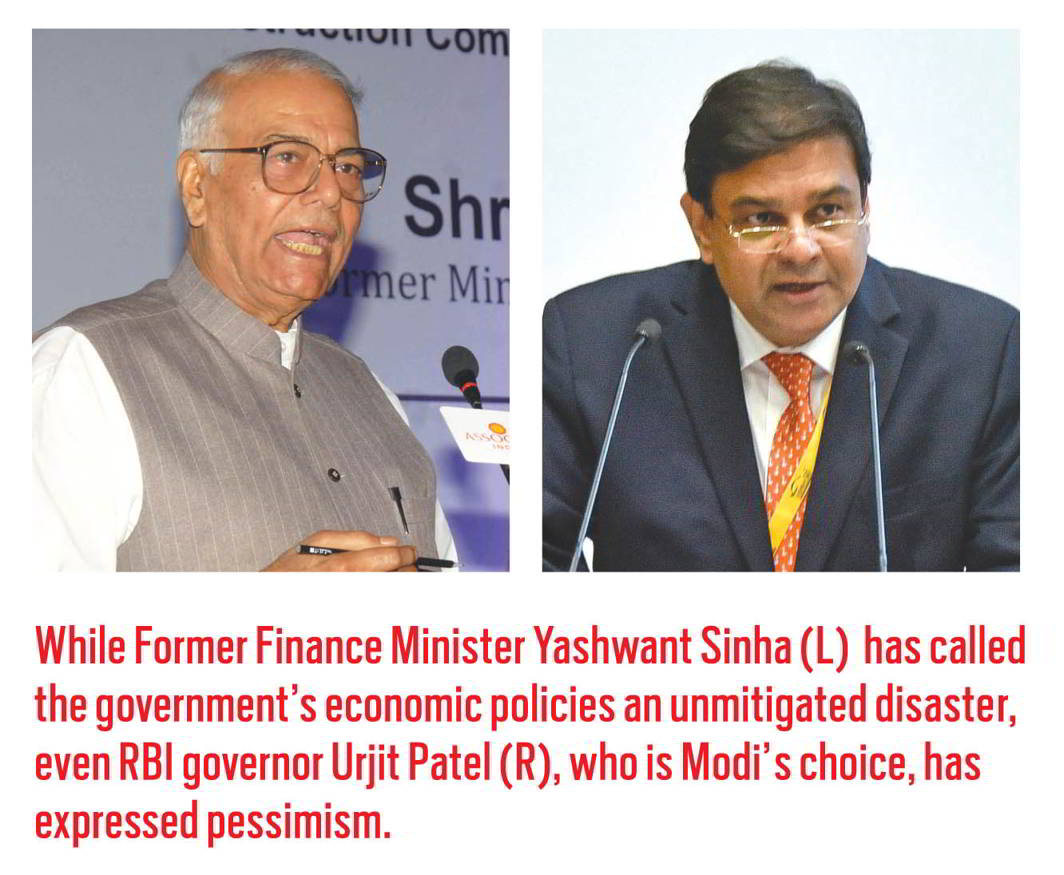

Today, many of Modi’s well-wishers and former allies and elder statesmen of his own party are sounding alarms. Former Finance Minister Yashwant Sinha and former Disinvestment Minister Arun Shourie have called the government’s economic policies an unmitigated disaster which have not only put development in reverse gear but also created misery for farmers and the unorganised sector and small traders.

But these are big, prominent names and convenient targets for alt facts and troll brigades. More worrisome for the BJP government are critics who are not sitting ducks, like the RSS-affiliated Swadeshi Jagran Manch, the All India Kisan Sabha, the Bharatiya Mazdoor Sangh, (also affiliated with the RSS) and hundreds of thousands of farmers who have marched in protest in BJP-ruled states like Rajasthan, Uttar Pradesh, and Maharashtra. Textile and jewellery traders in Modi’s backyard, Surat and Ahmedabad, have also taken to the streets in mass protest. Their grievances, too, centre on falling farm incomes and the massive disruption in supply chains caused by demonetisation and the imposition of GST.

Allies like both factions of the Shiv Sena are mounting frontal, often crude attacks on the government’s economic policies with no holds barred. And some media outlets whose promoters are recognised as being generally sympathetic to the BJP government with a decidedly soft corner for Modi, have become more strident in their reporting and criticism. Among them is the leading website Firstpost.

The prime minister appears to have taken this rising tide of critical opposition seriously. But being an eternal optimist, he recently derided his critics as “pessimists who spread despair”. But what was significant was his admission of a slight slowdown in the economy as well as glitches and problems with the GST system which he promised would be fixed.

He compared the pessimists to Shalya, the Kaurava charioteer in the Mahabharata who tried to paint a negative picture of the raging battle against the Pandavas. In his widely reported speech, the indefatigable Modi tried to put a positive spin on the economy, still hanging on to his promise of acchey din, but a friendly website took him to task in the very headline to that story, a sentiment echoed by many other several analysts: “PM’s data is impressive but it’s selective and fails to answer tough questions.”

Little did we think that Modi, with his uncanny instinct for kicking so accurately at the target, would ever score a goal against himself and face an economic slowdown circa 2008-2010

One reason for that is that among the “pessimists” is none other than the Reserve Bank of India headed by Modi’s own choice for governor, Urjit Patel. You need not turn to any newspaper or media source for details. Go straight to the RBI website and click on the “Fourth Bi-monthly Monetary Policy Statement, 2017-18 Resolution of the Monetary Policy Committee (MPC) Reserve Bank of India.”

It says in no uncertain terms that while the world economy is on the upswing following the terrible recession years, the Indian economy, which was among the fastest growing in the world, has been unable to take advantage of this. Here are highlights of the report:

- Since the MPC’s meeting in August 2017, global economic activity has strengthened further and become broad-based. Among advanced economies (AEs), the US has continued to expand with revised Q2 GDP growing at its strongest pace in more than two years, supported by robust consumer spending and business fixed investment. The Euro area purchasing managers’ index (PMI) for manufacturing soared to its highest reading in more than six years. The Japanese economy continued on a path of healthy expansion despite a downward revision in growth since March 2017 on weaker than expected capital expenditure.

- The latest assessment by the World Trade Organisation (WTO) indicates a significant improvement in global trade in 2017 over the lacklustre growth in 2016, backed by a resurgence of Asian trade flows and rising imports by North America.

- INDIA: On the domestic (India) front, real gross value added (GVA) growth slowed significantly in Q1 of 2017-18, cushioned partly by the extensive front-loading of expenditure by the central government. GVA growth in agriculture and allied activities slackened quarter-on-quarter in the usual first quarter moderation, partly reflecting deceleration in the growth of livestock products, forestry and fisheries. Industrial sector GVA growth fell sequentially as well as on a year-on-year basis. The manufacturing sector—the dominant component of industrial GVA—grew by 1.2 percent, the lowest in the last 20 quarters. The mining sector, which showed signs of improvement in the second half of 2016-17, entered into contraction mode again in Q1 of 2017-18, on account of a decline in coal production and subdued crude oil production. Of the constituents of aggregate demand, growth in private consumption expenditure was at a six-quarter low in Q1 of 2017-18. Gross fixed capital formation exhibited a modest recovery in Q1 in contrast to a contraction in the preceding quarter. (My italics)

- The index of industrial production (IIP) recovered marginally in July 2017 from the contraction in June on the back of a recovery in mining, quarrying and electricity generation. However, manufacturing remained weak. In terms of the use-based classification, contraction in capital goods, intermediate goods and consumer durables pulled down overall IIP growth.

Long queues in Allahabad to exchange old currency notes following demonetisation in November 2016. Photo: UNI - On the services side, the picture remained mixed. Many indicators pointed to improved performance even as the services PMI continued in the contraction zone in August due to low new orders. In the construction segment, steel consumption was robust. In the transportation sector, sales of commercial and passenger vehicles as well as two and three-wheelers, railway freight traffic and international air passenger traffic showed significant upticks. However, cement production, cargo handled at major ports, domestic air freight and passenger traffic showed weak performance.

- Retail inflation measured by year-on-year change in the consumer price index (CPI) edged up sequentially in July and August to reach a five month high, due entirely to a sharp pick up in momentum as the favourable base effect tapered off in July and disappeared in August. CPI inflation excluding food and fuel also increased sharply in July and further in August, reversing from its trough in June 2017.

- India’s export growth continued to be lower than that of other emerging economies such as Brazil, Indonesia, South Korea, Turkey and Vietnam, some of which have benefited from the global commodity price rebound. Import growth remained in double-digits for the eighth successive month in August and was fairly broad-based. The sharper increase in imports relative to exports resulted in a widening of the current account deficit in Q1 of 2017-18, even as net services exports and remittances picked up.

Being an eternal optimist, Modi recently derided his critics as “pessimists who spread despair”. But what was significant was his admission of a slight slowdown in the economy as well as glitches with the GST system

- Outlook: In August, headline inflation was projected at 3 percent in Q2 and 4.0-4.5 percent in the second half of 2017-18. Actual inflation outcomes so far have been broadly in line with projections, though the extent of the rise in inflation excluding food and fuel has been somewhat higher than expected. Taking into account these factors, inflation is expected to rise from its current level and range between 4.2-4.6 percent in the second half of this year.

- Turning to growth projections, the loss of momentum in Q1 of 2017-18 and the first advance estimates of kharif foodgrains production are early setbacks that impart a downside to the outlook. The implementation of the GST so far also appears to have had an adverse impact, rendering prospects for the manufacturing sector uncertain in the short term. This may further delay the revival of investment activity, which is already hampered by stressed balance sheets of banks and corporates. Consumer confidence and overall business assessment of the manufacturing and services sectors surveyed by the Reserve Bank weakened in Q2 of 2017-18 (My italics); on the positive side, firms expect a significant improvement in business sentiment in Q3. Taking into account the above factors, the projection of real GVA growth for 2017-18 has been revised down to 6.7 percent from the August 2017 projection of 7.3 percent.

- Imparting an upside to this baseline, household consumption demand may get a boost from upward salary and allowances revisions by states. Teething problems linked to the GST and bandwidth constraints may get resolved relatively soon, allowing growth to accelerate in H2. On the downside, a faster than expected rise in input costs and lack of pricing power may put further pressure on corporate margins, affecting value added by industry. Moreover, consumer confidence of households polled in the Reserve Bank’s survey has weakened in terms of the outlook on employment, income, prices faced and spending incurred.

- The MPC reiterated that it is imperative to reinvigorate investment activity which, in turn, would revive the demand for bank credit by industry as existing capacities get utilised and the requirements of new capacity open up to be financed. Recapitalising public sector banks adequately will ensure that credit flows to the productive sectors are not impeded and growth impulses not restrained. In addition, the following measures could be undertaken to support growth: a concerted drive to close the severe infrastructure gap; restarting stalled investment projects, particularly in the public sector; enhancing ease of doing business, including by further simplification of the GST; and ensuring faster rollout of the affordable housing programme with time-bound single-window clearances and rationalisation of excessively high stamp duties by states.

In other words, the MPC is saying that India is lagging behind because the government tried to fix something that wasn’t broken and wound up making things worse which now needs to be fixed if we are to get out of the crisis. And it pulls no punches on GST. This is not Yashwant Sinha or Shourie speaking. This is the Voice of RBI.

—Inderjit Badhwar is Editor-in-Chief, India Legal.

He can be reached [email protected]